Review Article

Volume-1 Issue-1, 2025

Infuential Factors of Online Purchase Intention in Financial Industry: A Perspective from an Emerging Economy

-

Received Date: August 03, 2025

-

Accepted Date: August 22, 2025

-

Published Date: August 29, 2025

Journal Information

Abstract

While extensive research of consumer intention on the online purchase has been carried out, little has been dis cussed about how product category may signi cantly in uence purchase intention. As numerous studies have an alyzed key drivers that a ect customer intention to purchase online nancial services, the level of perceived nancial value and risk in real would make the online purchase a less competitive choice. is study investi gates the direct e ects of four key factors, including prod uct features, nancial needs, institutional reputation, and government regulations, on online purchase intention in nancial industry, and the mediating roles of consumers’ perception in the above relationship. A structured ques tionnaire was designed, and survey data were collected from 218 respondents through various social media in China. e results indicate that each of the four inuen tial factors has a positive e ect on online purchase inten tion. Meanwhile, the perceived value positively mediates the e ect of the four inuential factors on purchase inten tion, while the purchase risk negatively mediates the ef fect on purchase intention. e ndings suggested that in order to attract more consumers to purchase online nancial services in an emerging economy, managers should focus on brand establishment, supervision im provement, and real-time customer engagement. Mean while, policy makers should develop regulations and poli cies to help ensure the safety of consumer transactions in e-commerce. Without these legal protections, consumers would be su ering from illicit activities that put their per sonal nances and privacy at risk.

Key words

Online Purchase Intention; Perceived Value; Perceived Risk; Product Features; Financial Needs; Insti tutional Reputation; Government Regulations

|

Research Items |

Factor Loading |

AVE |

CR |

Cronbach’s α |

|

Product Features |

0.792 ~ 0.841 |

0.665 |

0.856 |

0.858 |

|

Finance Needs |

0.795 ~ 0.821 |

0.657 |

0.852 |

0.867 |

|

Institutional Reputation |

0.777 ~ 0.850 |

0.661 |

0.854 |

0.862 |

|

Government Regulations |

0.808 ~ 0.829 |

0.665 |

0.856 |

0.893 |

|

Perceived Value |

0.746 ~ 0.836 |

0.615 |

0.827 |

0.808 |

|

Perceived Risk |

0.731 ~ 0.801 |

0.603 |

0.820 |

0.791 |

|

Purchase Intention |

0.713 ~ 0.826 |

0.585 |

0.808 |

0.845 |

|

Hypothesis/ Path |

Estimate |

t |

p-value |

|

H1: Product Features à Purchase Intention |

0.098 |

2.902 |

0.011 |

|

H2: Finance Needs à Purchase Intention |

0.113 |

3.506 |

0.023 |

|

H3: Institutional Reputation à Purchase Intention |

0.086 |

3.229 |

0.018 |

|

H4: Government Regulations à Purchase Intention |

0.376 |

6.424 |

0.037 |

|

Mediating Effect of Perceived Value à Purchase Intention H5a: Product Features Mediating Effect of Perceived Risk à Purchase Intention |

Coeff 0.2548 Coeff |

Coeff of PV 0.2594 Coeff of PR |

Indirect |

|

H6a: Product Features |

0.2548 |

-0.2292 |

0.0661 |

|

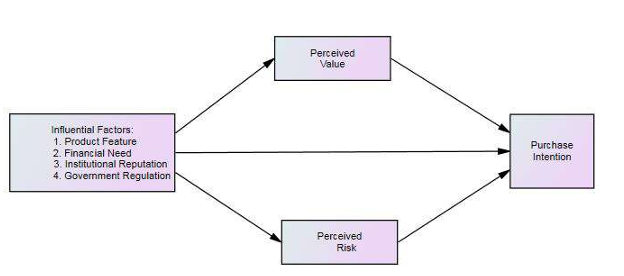

| Figure 1: Conceptual Framework |

|

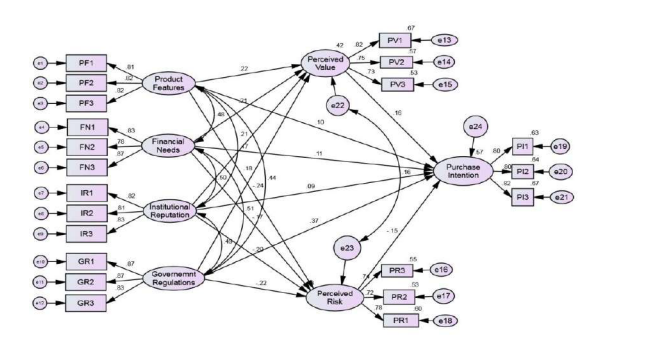

| Figure 2:Summary of results in hypothesized structural model (standardized) |

Introduction

Information system innovativeness generates online plat forms for businesses and the impact of e commerce is the posi tive contribution to online shopping [1]. As consumer buying decisions are largely dependent on the consumer behavior, there are great s in purchasing t products or services. In this regard, a powerful application of e-commerce in the l services industry can also more products and services. r and deliver t the viable commer cial mediums, the advantages of accessibility, convenience, and the result of cost saving would be appreciated by both businesses and consumers. Subsequently, the consumers most likely increase purchase intentions

Financial institutions have been d by the widespread use of the Internet in the planning and purchasing of financial services. Particularly, the COVID-19 pandemic and the need for social distancing have boosted the usage of online nancial services. Logically, purchase intentions will generally increase for those who need financial management or buy products and services while the time-consuming purchase process might considerably decrease. However, merchandises, on one hand, need more detailed information and therefore customers prefer personal interaction for their financial managements. On the other hand, consumers be haved much more carefully and conservatively with respect to the new Internet opportunities due to the concerns that there were technical and institutional obstacles related to informa tion security that would have to be solved. In addition, people around the world are still coping with the fear of the last the financial crisis, which caused massive distrust in the stability of governmental institutions as well as the respon sibility of those who manage the money of individuals and corporations. Consequently, it was not necessarily imperative for consumers to advance quickly towards Intent-based ser vices.

E commerce creates opportunities as well as challenges for financial businesses. Benifits of online services provided by financial institutions have been greatly recognized by the Amer ican Bankers Association. With the IT development and appli cation, customers enjoy instant access to relevant products and services while institutions have opportunities to expand markets and there profits

By analyzing the influential factors that have significantly impacts on the online purchase intention in financial industry, this study enhances the existing literature on the role of purchase perception (i.e. purchase value and risk) in shaping consumer purchase intention in e commerce, as well as intro duces consumer perception as a meditating factor to infulence consumers' purchase intention. Amidst the evolving landscape of e-commerce and consumer behaviors, gaps per sist in understanding the determinants of online purchase in tention, particularly within the financial industry. This study aims to address this research gap by comprehensively examin ing the factors infuluencing online purchase intention in the financial sector and exploring the mediating role of consumer perception.

The primary objectives are twofold:firstly, to investigate the infulential factors shaping online purchase intention, and se condly, to explore the mediating role of consumer perception. Grounded in established theories such as the Theory of Planned Behavior and Stimulus-Organism-Response model, the theoretical framework provides a structured approach to conceptualize the relationships between independent vari ables (product features,financial needs, institutional reputa tion, government regulations), the mediating variable (con sumer perception), and the dependent variable (purchase in tention). By achieving these objectives and leveraging this the oretical framework, this study aims to deepen our understand ing of consumer behavior in the context of online financial services, offering valuable insights for both practitioners and researchers alike.

Theoretical Background and HypothesesThe study explores purchase intention by utilizing theories in cluding the Theory of Planned Behavior (TPB) and the Stimu lus-Organism-Response (SOR) model. Recent research is inte grated to offer contemporary insights into factors shaping on line purchase intention, including subjective norms, per ceived usefulness, and product features. This study seeks to establish a robust theoretical groundwork and spotlight the latest trends in consumer behavior analysis. Additionally, this study aims to evaluate the impacts of product features, financial needs, institutional reputation, and government regula tions on consumers' online purchase intention within the financial services sector. Furthermore, it investigates the medi ating role of consumer perception, encompassing both perceived value and perceived risk, in shaping this relationship.

The conceptual research model, illustrated in Figure 1, out lines the dynamic interplay between these influential factors and consumer behavior in digital financial transactions Through this analysis, this study fosters a deeper understand ing of consumer decision-making processes in the digital financial landscape.

Online Purchase Intention on Financial IndustryPurchase behavior can be predicted through intentions [2]. Throughout the purchasing journey, consumer intention in tricately intertwines with consumption preferences, alongside factors like time and monetary investments [3]. Recent scho larly investigations have meticulously examined the complexi ties of online purchasing behavior within the digital financial sector, shedding light on the myriad factors infuluencing con sumer intentions. Research conducted by [4] has probed the determinants of online purchase intention, offering nuanced perspectives across diverse financial landscapes. Additionally, Binh Nguyen Thi et al. [5] explored the preferences of Genera tion Y and Z consumers in online services, while Khatoon et al. [6] scrutinized the factors shaping online purchase inten tion in the banking sector. These studies collectively enrich our understanding of consumer behavior in digital services, providing valuable insights into the decision-making processes underlying online purchases.

Online Purchase Intention and Product FeaturesBeneke et al. reference [7] explored how consumers perceive the value of products, emphasizing its crucial role in their purchase decisions. Their study highlighted how consumers' perceptions of value influence their willingness to buy andtheir assessment of prices. Other studies have also examined the relationships between product characteristics like quality and price, revealing their impact on consumer purchase inten tions [8,9].

When consumers consider purchasing a product, they typical ly focus on its features and quality, which greatly infulence their perception of its value. However, evaluating the quality of online financial services presents a unique challenge due to their intangible nature. Unlike tangible products, consumers evaluate online financial services based on the benifits they provide, such as additional income and risk mitigation. Consequently, consumers assess the value of online financial products based on their utility rather than tangible attributes Therefore, this paper proposed

H1: Product Features affect online purchase intention in financial industry

Online Purchase Intention and Financial NeedsTechnological progress has significantly enhanced the financial sector, facilitating easier access to financial services for consumers. These services play a pivotal role in aiding individ uals in managing their financial prudently and protecting themselves from unforeseen events. the COVID-19 pandemic and the imperative for social distancing have further pro pelled the utilization of online financial service. The height ened demand underscores the growing dependence on digital platforms for financial transactions, emphasizing the pivotal role of technology in reshaping both consumer behavior and industry dynamics. A survey released in 2020 by ESET [1] showed that in the US 65% of people use at least one Fin tech app or platform and 85% use either banking apps or on line banking platforms.

Another survey released in mid-2020 by KPMG [1] showed that the online access of financial planning services has accel erated during the lockdown. At the same time, a global survey conducted in 2020 by McKinsey [2] also indicated that the use of cash is decreasing and digital forms of transaction are increasing globally. While consumers expect to increase their reliance on online financial services to improve their financial health that would support their better selves, they will look for financial institutions which take a proactive ap proach and keep their customers informed about their invest ments in security.

The tendency is dramatically increasing the number of online users and the variety of services available provided by the financial institutions. Therefore, this paper proposed

H2: Financial needs affect online purchase intention in financial industry

Online Purchase Intention and Institutional ReputationFinancial products often entail intricate features and may pose challenges in comprehension for consumers due to their complexity. Inadequate access to comprehensive information further complicates decision-making processes, leaving con sumers uncertain about selecting the most suitable option. To address this issue and safeguard consumer interests, it is im perative to help them with sufficient resources to make in formed decisions. Enhanced transparency through disclosures emerges as a crucial strategy in strengthening consumer trust by offereing greater accountability and legitimacy [10]. By providing clear and comprehensive disclosures, financial institutions can bridge the information gap, empowering con sumers to make well-informed choices and fostering trust in the financial products and services they offer

Trust plays a vital role in the relationship between perceived online interactivity and purchase intention [11]. Numerous studies indicated that trust in e commerce enables online re tailers to achieve reputation and positive consequences on their performance [12,13]. Reputation is a significant factor to determine trust [10], and excellent reputation strengthen online shopping trust [14,15]. Reputation can be represented by brand and website image that consumers can easily obtain. Brand determines consumer engagement and in turn has an impact on brand trust, while Website image has a facilitating impact on perceived security and trust. Moreover, as con sumers concern about financial security that shape their atti tudes and trust towards a website, an online retailer’s positive reputation may diminish the risks and bring about trust [16,17]. Therefore, this paper proposed that:

H3: Institutional Reputation affects online purchase intention in financial industry

Online Purchase Intention and Government RegulationsIn terms of the perceptions of the consumer regarding Internet as a marketplace, Bhatnagar et al. [3] found that online financial services are still seen as a risky instrument, and such risk perception outweighs the convenience that it offers. The risks to security and integrity such as fraud and privacy issue may worsen if proper safeguards and regulations are not put into practice. In this regard, government regulations play a crucial role between consumers and financial institutions. Laws enforcement and regulations help hold companies ac countable and give more protection to people purchasing financial services, Which can increase consumer confidence

- Refer to https://mma.prnewswire.com/media/1453186/ESET_1.pdf?p=pdf

- Refer to https://home.kpmg/au/en/home/media/press-releases/2020/07/four-hs-consumers-prefer-digital-financial-services-covid-19-study-8-july-2020.html

- Refer to https://www.mckinsey.com/industries/financial-services/our-insights/a-global-view-of-financial-life-during-covid-19

Online financial services are fundamentally different from most other economic transactions. To some extent, the con sumers need to have trust and confidence in the products and the companies when making decisions. While the lack of trust and confidence can be regarded as a market failure, regula tions play a legitimate role to correct the failure and have the potential to enhance consumer trust and confidence [18]. Therefore, this paper proposed

H4: Government Regulations affect online purchase intention in financial industry

The Mediating Variable: Consumer PerceptionShopping online is perceived to be risky due to the con sumers’ belief regarding whether or not the product would function according to their expectations. Stimulus-Organis m-Response (SOR) model suggested that the occurrence of purchase behavior go through product category at the beginn ing, and then bring about some psychological adjustments through experience. When positive signals appear in this psy chological change, the actual purchase behavior will be deter mined by the subjective perception [19]. Analogously apply ing the SOR model to online purchase intention in the cial services industry, three phases are motivation, perception and decision. Alternatively, the theory of planned behavior (TPB) illustrates that the primary factors of purchase inten tions are governed by the attitude toward the behavior, the subject norms and the perceived behavioral control [2].

MotivationThe most crucial buying motive in a purchase for most of the customers is desire for financial gain. To motivate customers, financial institutions have to provide clear information re garding the advantages of the product, especially the benifits convenience, efficiency, high returns, and risk warnings. Per ception. Once identifying the benefits customers perceive to obtain in many ways while purchasing online financial prod ucts (e.g. Internet funds), these past experiences have a cer tain level of psychological impact on customers and turn into a strong stimulus [20]. Consumers are more likely to process stimulus that has relevance to buy Internet funds.

In addition, institutional features also play a driving factor in facilitating trade on the e commerce platform. Studies indicated that trust is a determinant element for consumers in rela tions to online purchase intention [21] [22]. Perceived institu tional assurance operates as a trust-building mechanism for reducing the risks [23]. Outstanding reputation therefore strengthens online shopping trust and brand reliability has significantly effectsof each experience on purchase decisions [24]. Decision. After through the stage of expoure and attentions to the stimulit infuluenced by unique needs and experi ences, consumers will be drawn to become highly selective and finally decide to purchase [20]. The purchase behavior occurs

The vital aspect of the conceptualization of purchase inten tion is that consumers choose actions to maximize the desired consequences and minimize undesired outcomes [25]. For on line purchasing behavior in financial services, consumer per ception comes from the response to external stimuli and deci sion making process involves internal cognitions state, reflectsing on the consumer perceived value, characteristics of prod ucts or services, the financial needs and planning, institution ai features, and current status of financial industry.

Perceived ValuePerceived value is one of the most determinant drivers that form consumer perceptions toward purchase intention. Com pared to the traditional mode of shopping, online purchase in deed provides consumers with perceived value, including con venience, cost saving, time saving [26]. Price fairness and quality also play the key roles with regard to tangible prod ucts to influence perceived value that may lead to repurchase intention [27]. These benfits perceived by customers will re sult in high satisfaction and eventually loyalty [28,29] [30]. Similarly, the more the positive experiences customers have in financial services, the higher the consumers’ perceived value. Therefore, this study proposed that:

H5a – H5d: Perceived Value has mediating effects of four influential factors (i.e. Product Feature, Finan cial Needs, Institutional Reputation, and Government Regulations) on online purchase intention in financial industry

Perceived RiskThe desired outcome of a purchase decision is expected to be positively satisfied However, the actual perception of goods and services in the process of selection is not always positive but strongly aware of the potential risks for consumers while purchasing online financial products and services. When the purchase intention moves from the potential negative conse quences to a certain degree of uncertainty, consumers will feel the perceived risk even if they have a strong willingness to buy [31].

Perceived risk is an assessment with considerations of subjec tive perceptions of risk and value judgments [32]. Before us ing the merchandizes, purchase intention is determined through subjective evaluations combined with prior experi ence and judgment of the possible loss. Once the subjective evaluation is damaged, consumers inevitably perceive disap pointment or loss and perceived risk incurs. Numerous studies in relation to online purchase illustrated the impor tant negative relationships between perceived risk and purchase intention from different perspectives, including product evaluation [33], brand effect [24], website reputation [22], familiarity [34], and social norms [35].

The online financial services provided by the financial indus try through internet platform are a novel way for consumers. Consumers make a purchase because they perceive benefits including convenience, cost savings, and a variety of products [36]. However, compared to the traditional mode with much paperwork to do, online purchase may perceive more risks for conservative customers. Studies suggested that in order to attract more customers to use online purchase,financial insti tution should minimize the potential risks through optimal service quality and customer reassurances [7].Therefore, this paper proposed

H6a-H6d: Perceived Risk has mediating effects of four influential factors (i.e. Product Feature, Financial Needs, Institutional Reputation, and Government Regulations) on online purchase intention in financial industry

Research Method

Construct Operationalization and Questionnaire DevelopmentLiterature review and variable discussion were carried out in order to operationalize the constructs and build the question naire. As each construct was measured by 3 items, this instru ment contained seven constructs with total 21 items. Five- point Likert’s scale was used, ranking from 1 (strongly disa gree) to 5 (strongly agree).

For measurement model, this paper used several criteria to measure the reliability and validity were examined [37]. The first criterion is Cronbach’s alpha coefficient, which should be higher than 0.6 to confirm the internal consistency of the research construct.The value of standardized factor loadings should be above 0.5. In addition, Bartlett’s test as well as the Kaiser-Meier-Olkin Measure of Sampling Adequacy (K MO-MSA) are examined. If Bartlett’s Test is significant and the value of KMO-MSA is greater than .50, this is considered an indication that it is appropriate to factor analyzing the ma trix.

The next criterion is to assess the convergent validity by the average variance extracted (AVE), which should be greater than 0.5 to assure that the latent variables can explain more than average [38]. The final criterion is the composite reliabili ty (CR), which should be greater than 0.7 to confirm that the variance shared by the respective indicators is robust. Hair et al. [37] also suggested that the value of AVE was above 0.5, and CR index was above the recommended value of 0.7.

For structural model, the path analysis is performed with two steps to assess the roles of perceived value and perceived risk as the mediating variables between each of the four infuluential factors and online purchase intention. Step one is to examine the direct effect of the four infuluential factors on online purchase intention, respectively. SPSS AMOS will be adopted. Step two is to evaluate if the path between each of the four infuluential factors and online purchase intention after the inclu sion of the perceived value and perceived risk constructs, re spectively. The indirect effects can be assessed by the PRO CESS Template Model 4 [39].

Data Collection and Analysis TechniqueThe sampling method employed in this study involved the de sign and distribution of a structured questionnaire to poten tial participants, with an emphasis on leveraging various so cial media platforms for recruitment. Specifically, the re searchers utilized social media channels to reach out to indivi duals in China and invite them to participate in the survey by filling out an internet-based questionnaire. Initially, 300 ques tionnaires were distributed, and 218 responses were deemed suitable for analysis, based on statistical and practical factors.

In terms of statistical principles, Hair et al. [40] suggests that a sample size ranging from 100 to 200 respondents is general ly sufficient for yielding reliable estimates of population pa rameters. Therefore the decision to include 218 respondents in this study aligns with established guidelines for sample size determination. Furthermore, from a practical standpoint, the scholars likely encountered limitations or challenges during the data collection process that infuluenced the final sample size. These may include factors such as response rates, data quality, or demographic representation. Despite these poten tial biases, the sample size of 218 respondents strikes a bal ance between statistical robustness and practical feasibility.

For 218 valid respondents, 114 were male (52.3%) and 104 were female (45.9). Most respondents were aged 31-40with to tal 66 (30.03%),and 109 (50.0%) obtained Bachelor's degree in college. Annual income over 200,000 RMB were 54 (24.8%).

Result and Analysis

This study conducted factor analysis and to ensure the dimen sion and Cronbach’s alpha tests to see if the survey is reli able. Table 1 shows that factor loading of all the questionnaire items are higher than 0.7 (0.713 ~ 0.841). Almost all Cron bach’s alpha of research items are higher than 0.8 (0.808 ~ 0.893) except one (i.e. perceived risk= 0.791), which almost all exceed the generally accepted guideline from Hair et al. [37]. The value of KMO (0.894) and Bartlett’s Test (p< 0.000) also indicate that the factor analysis is useful. e paper ap propriately concluded that all of the questionnaire items showed high degree of internal consistency and their factors are appropriate to be used for further analysis.

In Table 1, the values of all CR are ranged from 0.808 to 0.856, which are much higher than the benchmark of 0.5 as re commended. The AVEs of the constructs are ranged from 0.585 to 0.665, which are above the recommended value 0.5. The correlation among the constructs were all below 0.85, which means that the model has no discriminant validi ty problem.

The model fit indices (Chi-square/df= 1.042, p-value = 0.335; RMSEA = 0.014; GFI = 0.931; AGFI = 0.905; CFI = 0.997) are satisfactory. The empirical results in Figure2show that Prod uct Feature (β=0.098; p< 0.05) has a significant impact on the Purchase Intention. In addition, Financial Needs (β=0.113; p< 0.05) has a significant impact on the Purchase Intention. Furthermore, both Institutional Reputation (β=0.086; p< 0.05) and Government Regulations (β=0.376; p< 0.05) have significant influences on the Purchase Intention. The outcomes support H1, H2, H3, and H4.

Meanwhile, in Table 2the indirect effects of these four influential on Purchase Intention that go through two mediators (i.e. Perceived Value and Perceived Risk) are statistically significant The value of the indirect effects of two mediators on Purchase Intention falls between lower and upper bound and 0 falls outside of the bound at 95% confidence intervals. Based on the Table 2, the meditating effects of Perceived Value has positively significant influence of the four influential factors on Purchase Intention, while the Perceived Risk has nega tively significant influence on the relationship between the influential factors and Purchase Intention. The hypotheses H5a-H6d are supported.

Discussion

With the dramatic development of information technology in recent years, online transactions have grown tremendously.The impact of external factors such as COVID-19 pandemic also plays one of the driving roles that facilitate this trend. A survey concluded that this pandemic has accelerated the shift towards more online purchases and the changes are likely to have lasting effects. The effects have been particularly significant for financial institutions as as online shopping has become the norms. Nevertheless, when managers around the world make the most of highly engaging online channels, financial institutions in emerging economies face more issues and chal lenges than in advanced markets.

From an academic viewpoint, while most of the existing re searches analyze the various impact factors on purchase inten tion without taking product category into consideration, this study found that consumers evaluate online financial prod ucts with more perspectives than ordinary mechanizes before making decisions to buy. In this context, the contribution of this paper is to cluster and attribute three of the four influential factors (i.e. product features, financial needs, and institutional reputation) as consumers’ cognitive perception, which can be fairly carried out in parallel with the implementation of regulations. In the meantime, the partial relationship analy sis is identified that both perceived value and perceived risk have mediating effects but go in opposite direction on the on line purchase intention.

Managerial ImplicationsThe positive and significant coefficients of path analysis be tween online purchase intention through mediating factors and the four infuluential factors have four managerial implica tions. First, the more positive features of products, the higher the value perceived by the customers. Financial institutions develop strategies to better understand the development of on line products in financial services. It should help identify the conditions under which some financial services are in demand, while others may offer a wide variety of features. Tar geting the product value will help to maximize the needs of users through customer-centered product design. Secondly, when product features match consumers’ needs, purchasing decisions are most likely made on the basis of institutional reputation. To win trust, financial institutions can make dis closer more meaningful for consumers to enhance the prod ucts values such as safe, convenience, quick service and so on. For the consumers who have less information or online purchasing experiences of financial services, reputation is the vital factor to influence purchase intention. Therefore, focus ing on brand establishment is the most important task of all in financial industry.

Thirdly, supervision improvement and real-time customer en gagement are efficient ways for financial institutions to build up reputation in financial industry. For the former, financial institutions either launch initiatives by themselves to improve governance, or reluctantly abide by the government regula tions, would help earn reputation [41]. For the latter, numer ous studies showed that establishing consumer’s engagement is beneficial for the company for it raises corporate reputation [42] and result in a remarkable relationship in form of com mitment, trust, and brand loyalty [43]. The real-time cus tomer engagement may provide impartial advice that will lead a customer through their journey while building trust in company’s brand.

Finally, government regulations can significantly affect the financial industry. The main regulatory body protecting inves tors from mismanagement and fraud encourages investor confidence and investment. In emerging markets such as China, The financial industry develops lag behind more developed economies largely due to outdated regulations. Thesituation can be observed from the samples collected in China, where most consumers are not satisfied with the current status of online financial services. Governments in emerging markets need to introduce regulatory reforms to promote growth and mitigate risk, including levels of financial inclusion and regulations surrounding financial services.

See at https://unctad.org/system/files/official-document/dtlstictinf2020d1_en.pdf

Conclusion and Limitations

The findings underscore actionable insights for both man agers and policymakers in navigating the evolving landscape of online financial services. For managers, the study illumi nates the significance of understanding consumer percep tions and preferences in designing and marketing online prod ucts effectively. It emphasizes the importance of product fea tures, institutional reputation, and regulatory compliance in fostering consumer trust and purchase intention. Managers are urged to prioritize customer-centric product design, en hance institutional transparency, and engage in proactive gov ernance to bolster reputation and consumer confidence. Moreover, the study underscores the pivotal role of real-time customer engagement in fostering brand loyalty and trust, ad vocating for investments in interactive platforms and person alized services.

On the policymaker front, the study emphasizes the criticality of regulatory reforms to stimulate growth and mitigate risks in emerging financial markets. Policymakers are urged to modernize regulatory frameworks to align with evolving consumer behaviors and technological advancements. This entails fostering financial inclusion, enhancing investor protec tion, and promoting innovation while safeguarding against potential risks. Moreover, the study highlights the need for policymakers to address challenges specific to emerging economies, such as outdated regulations and low financial literacy, By enacting forward-thinking policies and fostering a conducive regulatory environment, policymakers can catalyze the development of robust online financial ecosystems that benefits both consumers and bussynesses.

The limitations of this paper have three. The targeted country China is categorized as an emerging economy with a huge population. The sample size could be larger and therefore might turn out different results. Meanwhile, China has the most state-of-the-art online payment systems in the world. However, the financial system in China are not functioning well largely due to the fact that people are not aware of the benefits of financial services until recent years. Therefore additionally influential factors may be applicable. Finally, different industries with the same influential factors may lead to dif ferent outcomes, and therefore is recommended for future studies.

References

- Blake BF, Neuendorf KA, Valdiserri CM (2003) Innovative ness and variety of Internet shopping. Internet Research Elec tronic Networking Applications and Policy, 13: 156-69.

- Ajzen I (1991) The Theory of Planned Behaviour. Organiza tional Behaviour and Human Decision Processes, 50: 179-211

- Bhatnagar A, Misra SM, Rao RH (2000) On risk, conve nience, and Internet shopping behavior. Communications of the ACM, 43: 98-105.

- Dewi CK, Mohaidin Z, Murshid MA (2020) Determinants of online purchase intention: a PLS-SEM approach: evidence from Indonesia, Journal of Asia Business Studies, 14: 281-306.

- Binh Nguyen Thi, Thi Lan Anh Tran, Thi Thu Hien Tran, Phan Nhat Hang Tran, Minh Hieu Nguyen (2022) Factors influencing continuance intention of online shopping of genera tion Y and Z during the new normal in Vietnam, Cogent Busi ness & Management, 9.

- Khatoon S, Zhengliang X, Hussain H (2020) The Mediating Effect of Customer Satisfaction on the Relationship Between Electronic Banking Service Quality and Customer Purchase Intention: Evidence From the Qatar Banking Sector. Sage Open, 10.

- Beneke J, Flynn R, Greig T, Mukaiwa M (2013) The influence of perceived product quality, relative price and risk on customer value and willingness to buy: a study of private label merchandise. Journal of Product & Brand Management, 22: 218-28.

- Haryanto B, Purwanto D, Dewi AS, Cahyono E (2019) Product types in moderating the process of buying street foods. Journal of Asia Business Studies, 13: 525-42.

- Setiawan MM, Haryanto B (2014) e antecedent variables of attitude in forming intention to switch smartphone (the survey study: Samsung brand in Surakarta). European Jour nal of Business and Social Sciences, 3: 126-35

- Yahia IB, Al-Neama N, Kerbache L (2018) Investigating the drivers for social commerce in social media platforms: im portance of trust, social support and the platform perceived usage. J. Retail. Consum. Serv, 41: 11–9.

- Hansen JM, Saridakis G, Benson V (2018) Risk, trust, and the interaction of perceived ease of use and behavioral control in predicting consumers’ use of social media for transactions. Comput. Hum. Behav, 80: 197-206.

- Pratono AH (2018) From social network to mance: the mediating effect of trust, selling capability and pricing capability. Manag. Res. Rev, 41: 680-700.

- López-Miguens MJ, Vázquez EG (2017) An integral mod el of e-loyalty from the consumer’s perspective. Comput. Hum. Behav, 72: 397-411.

- Izogo EE, Jayawardhena C (2018) Online shopping experi ence in an emerging e-retailing market: towards a conceptual model. J. Consumer Behav, 17: 379-92.

- Chen X, Huang Q, Davison RM (2017) Economic and so cial satisfaction of buyers on consumer-to-consumer plat forms: the role of relational capital. Intern. J. Electron. Com merce, 21: 219-48.

- Walsh G, Schaarschmidt M, Ivens S (2017) s of cus tomer-based corporate reputation on perceived risk and rela tional outcomes: empirical evidence from gender moderation in fashion retailing. J. Product BrandManag, 26: 227-38.

- Zhang M, Ren C, Wang GA, He Z (2018) The impact of channel integration on consumer responses in omni-channel retailing: the mediating effect of consumer empowerment. Electron. Commerce Res. Appl, 28: 181-93.

- Llewellyn DT (2005) Trust and confidence in financial ser vices: a strategic challenge. Journal of Financial Regulation and Compliance, 13: 333-46.

- Kawaf F, Tagg S (2012) Online shopping environments in fashion shopping: an S-O-R based review. Marketing Review, 12: 161-80

- Solomon M, Bamossy G, Askegaard S, Hogg MK (2010) Consumer Behaviour: A European Perspective. Harlow: Pear son Education.

- Sisson DC (2017) Inauthentic communication, organiza tion-public relationships, and trust: a content analysis of online astroturfing news coverage, Public Relat, Rev, 43: 788-95

- Sullivan YW, Kim DJ (2018) Assessing the s of con sumers’ product evaluations and trust on repurchase inten tion in e-commerce environments. Intern. J. Inform. Manag, 39: 199-219.

- Malhotra N, Sahadev S, Purani K (2017) Psychological contract violation and customer intention to reuse online re tailers: exploring mediating and moderating mechanisms. J. Bus. Res, 75: 17-28.

- Bleier A, Harmeling CM, Palmatier RW (2019) Creating effective online customer experiences. J. Relationship Mark, 83: 98-119.

- Kumar V, Reinartz W (2016) Creating Enduring Cus tomer Value. Journal of Marketing, 80: 36-68.

- Margherio L, (1998) e emerging digital economy. Secre tariat for Electronic Commerce, Washington.

- Toni D, Eberle L, Larentis F, Milan GS (2018) Antece dents of Perceived Value and Repurchase Intention of Organ ic Food, Journal of Food Products Marketing, 24: 456-75.

- Curtis T, Abratt R, Rhoades DL, Dion P (2011) Customer Loyalty, Repurchase and Satisfaction: A Meta-Analytical Re view. Journal of Consumer Satisfaction, Dissatisfaction and Complaining Behavior, 24

- Howat G, Assaker G (2013) The hierarchical effects of per ceived quality on perceived value, satisfaction, and loyalty: em pirical results from public, outdoor aquatic centres in Aus tralia. Sport Management Review, 16: 268-84.

- Yu HS, Zhang JJ, Kim DH, Chen KK, Henderson C, et al. (2014) Service quality, perceived value, customer satisfaction, and behavioral intention among s center members aged 60 years and over. Social Behavior and Personality, 42: 757-67.

- Stone RN, Grønhaug K (1993) Perceived Risk: Further Considerations for the Marketing Discipline, European Jour nal of Marketing, 27: 39-50.

- Skjong Rolf, Benedikte HW (2001) "Expert Judgment and Risk Perception." Paper presented at the Eleventh International Offshore and Polar Engineering Conference, Stavanger Norway.

- Han MC, Kim Y (2017) Why consumers hesitate to shop online: perceived risk and product involvement on Taobao. com. J. Promot. Manag, 23: 24-44.

- Gibreel O, AlOtaibi DA, Altmann J (2018) Social com merce development in emerging markets. Electron. Com merce Res. Appl, 27: 152-62.

- Xie Q, Song W, Peng X, Shabbir M (2017) Predictors for e-government adoption: integrating TAM, TPB, trust and per ceived risk. Electron. Lib, 35: 2-20.

- Ali Khatibi, Ahasanul Haque, Khaizurah Karim (2006) E- Commerce: A Study on Internet Shopping in Malaysia. Jour nal of Applied Sciences, 6: 696-705.

- Hair JF, Ringle CM, Sarstedt M (2011) PLS-SEM: Indeed a silver bullet. Journal of Marketing theory and Practice, 19: 139-52.

- Henseler J, Ringle CM, Sinkovics RR (2009) e use of partial least squares path modelling in international market ing. In New challenges to international marketing 277-319.

- Hayes AF (2017) Introduction to Mediation, Moderation, and Conditional Process Analysis: Second Edition: A Regres sion-Based Approach. New York, NY: Guilford Press.

- Hair JF, Howard MC, Nitzl C (2020) Assessing measure ment model quality in PLS-SEM using confirmatory com posite analysis. Journal of Business Research, 109: 101-10.

- Romero AG (2003) Integrity and good governance - repu tation risk in the public sector and financial institutions. Speech delivered on the occasion of the opening of the Sixth Biennial Regional Central Banks Legal Seminar, Willemstad, CuraÁao.

- Doorn J, Lemon KN, Mittal V, Nass S, Pick D, et al. (2010) Customer engagement behavior: Theroretical founda tions and research directions. Journal of Service Research, 13: 253-66.

- Brodie R, Hollebeek LD, Juroc B, Ilic A (2011) Customer Engagement: Conceptual Domain, Fundamental Proposi tions, and Implications for Research. Journal of Service Re search (JSR) 14: 252-71.

Artcle Information

Review Article

Received Date: August 03, 2025

Accepted Date: August 22, 2025

Published Date: August 29, 2025

Journal of Business Management and Economics Statistics

Volume 1 | Issue 1

Citation

Shimei Wen (2024) Inuential Factors of Online Purchase Intention in Financial Industry: A Perspective from an Emerging Economy. J Bus Manage Econ Stat 1: 105

Copyright

©2025 Shimei Wen. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

doi: jbme.2025.1.105